Different cultures have different days that are important to them. The Europeans don’t care about our Columbus Day, nor does the typical American even pause to think about Canadian Boxing Day. That’s easily understandable, as different world groups have unique reasons to remember special days.

But what about us? Collectively, we might be called the “Loosely Affiliated Group of Natural Gas Market Participants, Florida Chapter.” What holiday should we remember? Easy. We should care about Veterans Day. It is the number one holiday on our calendar.

On this holiday, it is important to remember the many folks that have protected our country through the years, sacrificing so much. But Veterans Day also roughly coincides with the last weekly natural gas storage build of the annual inventory season. Each week of the year, on Thursday, the EIA reports inventory builds and draws in the natural gas market. And, since the typical demand profile for natural gas is winter heavy and summer light, inventories build through the summer. If we were to look at a seasonal price chart of the natural gas market, we would find a rough correlation to the storage season – low prices in the summer as inventories build followed by higher prices during the winter as the market experiences periods of peak demand. (There are things that from year-to-year can disturb this seasonal pattern – hurricanes or economic “meltdowns”, for example – but the seasonal is still generally representative of the overall balance of gas supply and gas demand in the market.)

On this Veterans Day, the natural gas market finds itself at a bit of a crossroads. For months, the broad news media has been reporting on the development of unconventional supply sources – “shale plays” – in a broad swath of the midcontinent from Texas and Arkansas through to Pennsylvania and New York. New technologies have unlocked vast amounts of previously unavailable natural gas, causing a supply glut this year and drastically affecting the future supply-demand balance. Proven domestic reserves of natural gas have increased by 50% in the last two years.

These changes to the market have impacted price dramatically, pushing the price of cash natural gas in Louisiana to below $2.00/dekatherm in early September. But at that time, the curve of forward prices reflected a huge carry to the winter-time, typical of an over-supplied market. So although price was dirt cheap in the spot market, gas really couldn’t be bought in the forward market at a similar low price. But things change. Markets change. And now here we are….Veterans Day.

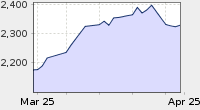

Since that point in September, the market has moved around a bunch. It rallied by almost $3.00, only to set back again under the pressure of mild weather and lack of early season heating demand. Now January gas is trading for $4.86/dekatherm on the NYMEX – on its face this looks to be around $3 dollars higher than that September low. But it is not. Because at the time that cash gas was below $2.00, the January NYMEX was trading for $5.00-5.25. So right now, the January market is at parity with its previous 2009 low.

Where it goes from here I guess no one knows. I have been watching, trading, and studying commodity markets for 15 years, and “no one knows” is one of the only things I know for certain. But let’s think briefly about the range of possible outcomes that the market could present to us. In the face of remarkably bearish fundamentals, the market remains around $5.00. Consider that until now the market has been presented with mild weather and building storages (remember Veterans Day?). But with the onset of more robust cold fronts and growing degree day counts, the market has the potential to rally. As I wrote in my last commentary, the two previous times this decade that the front month hit $2.75, within 12 months the market traded at above $9.00. The market will do whatever it has to in order to fool the majority.

Locking in a piece of fixed price at this level, one risks the chance that the market will fall to the sub-$3 level. But not locking in at this level is the equivalent to a bet that price WILL go down as we proceed into the winter supply drawing season. With Veteran’s Day upon us and the storage draws beginning, I don’t like the odds on that bet.

Tuesday, November 10, 2009

Tuesday, October 20, 2009

Changing the Energy Map

Technology Review has an interesting article here:

Experts now believe that the country has far more natural gas at its disposal than anyone thought three or four years ago. The revised estimates are largely due to advanced drilling techniques that make it economically feasible to extract the fuel from shale. And while the Marcellus is the most recently discovered and possibly the largest shale-gas deposit, others are scattered throughout the country. The U.S. consumes about 23 trillion cubic feet (TCF) of natural gas a year, according to the Department of Energy's Energy Information Agency (EIA). The Potential Gas Committee (PGC), an organization headquartered at the Colorado School of Mines, put the country's potential natural-gas resources at 1,836 TCF in a biennial assessment released in June. That's 39 percent higher than its estimate of two years earlier. Add to that the 238 TCF that the EIA has calculated in "proved reserves" (the gas that can be produced given existing economic conditions) and the PGC pegs the future supply at 2,074 TCF. In other words, there is enough natural gas to supply the country for 90 years at current consumption rates. Even if we used natural gas to totally replace coal in generating electricity, domestic supplies would last for 50 years.

Monday, September 21, 2009

Rediscovering Natural Gas

NPR's Morning Edition on the glut of shale gas hitting the market.

"I used to say the nation is awash in natural gas," Hefner says. "Now I say we're drowning in it."

One area getting new attention is the Marcellus basin, a 400-million-year-old shale formation stretching from New York to West Virginia. That basin alone is believed to hold as much as 500 trillion cubic feet of natural gas, the equivalent of about 80 billion barrels of oil. (There are also large shale gas basins in Texas, Wyoming, Arkansas and Michigan.) It is not clear how much of the shale gas is recoverable, but the new production techniques have boosted all previous estimates.

Shale formations are deep underground — 6,000 feet or more — and the rock is relatively impermeable. Deep drilling is expensive, and in the past the amount of gas that could be reached was not considered sufficient to justify the cost.

Sunday, September 20, 2009

The Dorian Gray Pill

Mostly, I try to post only market info on this site. But I can't resist. This op-ed is by a conservative economist that teaches at Harvard.

I am confident that you will find it thought provoking. Below is an excerpt, the whole article is HERE.

I am confident that you will find it thought provoking. Below is an excerpt, the whole article is HERE.

Imagine that someone invented a pill even better than the one I take. Let’s call it the Dorian Gray pill, after the Oscar Wilde character. Every day that you take the Dorian Gray, you will not die, get sick, or even age. Absolutely guaranteed. The catch? A year’s supply costs $150,000.

Anyone who is able to afford this new treatment can live forever. Certainly, Bill Gates can afford it. Most likely, thousands of upper-income Americans would gladly shell out $150,000 a year for immortality.

Most Americans, however, would not be so lucky. Because the price of these new pills well exceeds average income, it would be impossible to provide them for everyone, even if all the economy’s resources were devoted to producing Dorian Gray tablets.

So here is the hard question: How should we, as a society, decide who gets the benefits of this medical breakthrough? Are we going to be health care egalitarians and try to prohibit Bill Gates from using his wealth to outlive Joe Sixpack? Or are we going to learn to live (and die) with vast differences in health outcomes? Is there a middle way?

Thursday, September 17, 2009

Explaining the Irrational Exuberance of Natural Gas: De-constructing a Dead Cat Bounce

Since the last time I wrote an extended piece on this blog site, the market has moved significantly (56% higher than the low placed about 10 days ago). The market didn’t see this rally coming. And, searching for answers, analysts attempt to attribute a particular fundamental to what has transpired over the last 10 days. I don't think what has gone on is "fundamental" - as in supply and demand - at all. In my opinion, it is a dead-cat bounce.

This rally was a one of human emotion. It was caused by a blend of greed (or complacency) and fear. As the market fell, the front month price fell more significantly than the out months. This Rigzone article discusses that the steepness of the term structure contango was a four standard deviation event - meaning that the difference between the front month price and the out-month price is about as significant as it ever gets. Considering this, many shorts entered the market in the front month, knowing that the roll from month to month would credit their position and the term-structure "contango" would work in their favor.

These speculative positions in the market were short in the face of the lowest gas prices in a decade. But they were making money, so they remained short. And then….the market rallied 15 cents. Some of them – the recent entrants – were then holding losing (unprofitable) positions. Trading with a stop-loss discipline, they said “enough is enough” and blew out – they BOUGHT. This pushed the market higher, and took even more trader's positions into negative equity situations. As nervous or disciplined investors, THEY headed for the exits, too. They BOUGHT. And this forced the market higher still. At this point the market had rallied maybe 50 cents. At this point, the market move started to attract the hot money that looks for trends with velocity. This money wants to jump on the trending market’s bandwagon and ride that bandwagon for a significant and quick profit. So…the move higher created by nervous investors exiting shorts is exacerbated by new “hot money” longs. The market has ingested these new positions by adjusting price, and by now it is more than a dollar higher. And...here we stand. Such is the status of the natural gas market on September 16th.

These speculative positions in the market were short in the face of the lowest gas prices in a decade. But they were making money, so they remained short. And then….the market rallied 15 cents. Some of them – the recent entrants – were then holding losing (unprofitable) positions. Trading with a stop-loss discipline, they said “enough is enough” and blew out – they BOUGHT. This pushed the market higher, and took even more trader's positions into negative equity situations. As nervous or disciplined investors, THEY headed for the exits, too. They BOUGHT. And this forced the market higher still. At this point the market had rallied maybe 50 cents. At this point, the market move started to attract the hot money that looks for trends with velocity. This money wants to jump on the trending market’s bandwagon and ride that bandwagon for a significant and quick profit. So…the move higher created by nervous investors exiting shorts is exacerbated by new “hot money” longs. The market has ingested these new positions by adjusting price, and by now it is more than a dollar higher. And...here we stand. Such is the status of the natural gas market on September 16th.

Old trader types say “if you drop it far enough, even a dead cat will bounce.” It is because the steady move lower allows folks to get out of position – to blend greed and complacency and find them in an unmanageable position should the market stop behaving in such a convenient and predictable trend. I perceive the recent strength as a dead-cat bounce and I look for more downside as the market adjusts from the exuberance of the last 10 days.

Let’s not forget: Natural gas storages are full. Rig counts are down, and gas production numbers still relatively flat to prior years. There are new and significant sources of shale bed supply that are shell-shocking the market to a new reality, and the demand base is slow to evolve to these breakthroughs. These are all short-to-intermediate term bearish considerations.

As I wrote in my last market commentary extended post, the last two times that natural gas prices have been this cheap, things turned around quickly. People that actively manage energy price risk should consider buying a piece of product at historically low prices if it fits their needs. And while we all get nervous in this situation, after the market rallies 56% off the lows, it seems reasonable to wait for prices to adjust after such a dead-cat bounce.

Wednesday, September 16, 2009

One Year Post Lehman: "A Drunken Binge of Excess...is Over"

See the CNBC interview here.

“The West, especially the Anglo-Saxon economies, went on a drunken binge of excess consumption, leveraged up the eyeballs with totally inadequate savings,” Roach said. “It was reckless, irresponsible and it’s over,” he added.

Tuesday, September 15, 2009

Is NYMEX Natural Gas a "Bubble"

That is what Steven Schork says...here. (This article, from the Financial Times, is ABSOLUTELY worth the jump.)

"We stand by our words and our numbers. No doubt, gas is cheap. But, if there is no value, than cheap, in and of itself, is not a reason to own something. Back in the 1980s the Yugo GV was cheap also. The car was cheap for a reason. Its Soviet-bloc engineering (see today’s G.M.) exuded the feeling it was assembled at gunpoint1. Gas today is cheap for a reason.

There is too damn much of it. Over the weekend Alan Lammey at Natural Gas Week noted that ANR Storage was reported as 97.4% full, Sonat Storage was 97.3% full. Meanwhile, Texas Gas Storage was 96% full, Transco Storage was 83.3% full and Tennessee was estimated at 89% full… and it is only the middle of September for crying out loud."

Wednesday, September 9, 2009

Will the Demand for Assets Fall When the Baby Boomers Retire?

A new paper from the Congressional Budget Office states the following:

"...[will] the demand for assets, such as stocks and bonds, will fall after the retirement of the baby-boomer generation—the segment of the nation’s population born between 1946 and 1964, whose oldest members turned 62 in 2008. Some economists have warned of the possibility of a dramatic decline in demand as baby boomers sell off their assets to finance their retirement; they assert that the sell-off could cause a dramatic decline in prices. An evaluation of the evidence, however, indicates that such a dramatic decline in asset demand and prices is unlikely."

Do You Worry about how Your Spleen Works?

A spunky rebuke of Peak Oil theory is found in the Canadian National Post:

Note how the use of the term “skeptics” suggests that Peak Oil is the mainstream view, which it is not. The word also links unbelievers to beyond-the-pale climate change “skeptics.” Finally, the report suggests that these people are suggesting a “golden age of exploration and supply” although in fact the only relevant quote is from Peter Odell, professor emeritus of international energy studies at Erasmus University in Rotterdam, who merely says, “It’s an amazing turnaround from the gloom of the last 10 years. All these finds will take a long time to bring on stream, but it shows the industry is capable of finding more oil than it uses and shows we have not come to any peak.”

Peak Oil theory represents a combination of economic ignorance and moral rejection of markets as greed-driven and shortsighted. These all-too common attitudes usually go with a profound faith in effective government policy, despite the monumental weight of evidence to the contrary.

The seminal image for depletionists -as for apocalyptic climate change theorists — is that of the photo of the Earth taken from Apollo 17; seemingly dramatic confirmation of finite resources on a “small planet.” In fact, the interpretation of the Apollo picture is symptomatic of how far technology has outstripped our primitive assumptions about the way the world works. But then people don’t have to think about the vast, natural “extended order” of the economy any more than they have to worry about how their spleens work. (italics are mine)

Debate between economists and Peak Oilsters tends to be a dialogue of the deaf. Economists often seem to imagine that they are explaining a technical issue. They note that the alleged failure to “replace” production is in fact due to the way reserves are reported. They stress that startling new technologies –such as the ability to drill in thousands of metres of water to depths of more than 10,000 metres (as at Tiber), or 3-D computer seismic imaging, or horizontal drilling –are constantly finding new oil and gas, and producing more from old reservoirs.

Again, citing how often alarms over “the end of oil” have been sounded since 1880 holds no sway with Peaksters. Since they see oil supply as essentially “fixed” and economists as deluded and morally deficient, delays in the projected “crunch” will only make it all the more painful when it –inevitably –comes."

Sunday, September 6, 2009

Let's Be Practical

Barry Eichengreen, a professor at Cal-Berkeley, writes an essay in The National Interest about the future of economics after the fallout from the last year's crisis:

"...Work in economics, including the abstract model building in which theorists engage, will be guided more powerfully by this real-world observation. It is about time.

Should this reassure us that we can avoid another crisis? Alas, there is no such certainty. The only way of being certain that one will not fall down the stairs is to not get out of bed. But at least economists, having observed the history of accidents, will no longer recommend removing the handrail."

Saturday, September 5, 2009

Thursday, September 3, 2009

BP Finds Oil - Lots of It - 35,055 ft below the Earth's Surface

See all about it on Bloombergy TV:

Read All About It:

From the Wall Street Journal

From the Houston Chronicle

Hear All About:

On NPR's Marketplace

Read All About It:

From the Wall Street Journal

From the Houston Chronicle

Hear All About:

On NPR's Marketplace

Tuesday, September 1, 2009

Monday, August 31, 2009

The KNOWN UNKNOWNS

There is a famous Pentagon briefing that has been lampooned quite a bit. During this briefing Donald Rumsfeld steps to the podium to discuss the intelligence situation in Afganistan. He says:

"There are known knowns. These are things we know that we know. There are known unkowns. That is to say, there are things we know we don't know. But, there are also unknown unknowns. These are things we don't know we don't know."

He got a chuckle from some reporters. He got stares of confusion from others. As for me, I knew exactly what he was saying. And immediately I could relate it to my life. "Unknown Unknowns" in Secretary Rumsfeld's lingo, are things that we need to be worried about that we don't even know TO be worried about.

.

.

When driving down the road, you know to stay on the right side as you crest a hill. There could be a car coming the other way. (Since you knew to be cautious, that is an example of a known unknown.) But as you crest that same hill and fall into a sinkhole created by recent rainstorms, you experience an unknown unknown (you didn't even realize that you needed to be worried about such a problem).

.

.

As individuals that are affected by the energy markets, we are all impacted by known and unknown unknown variables. We are surrounded by known unknowns like hurricanes in the gulf or weekly storage inventory changes. And these make the market move. These variables have pushed the price of natural gas to 7-year lows. There are also unknown unknowns, like when the subprime mortgage snowball gained such inertia that a massive commodity deleveraging sell off took place (4Q 2009). The market did not even know to expect that one...it came out of nowhere, just like the sinkhole our car drove into in the previous paragraph. Unknown unknowns push the market much more violently and much more significantly when they appear. And no one can predict when they will arise and become important - that is the true nature and danger of an unknown unknown.

.

.

By this point, no doubt, my readers think I am as crazy as the reporters found Donnie Rumsfeld that day at the poduim. But one of my favorite quotes from Charles Dow will help tie this together.

"There is always a disposition in people's minds to think that existing conditions will be permanent. When the market is down and dull, it is hard to make people believe this is the prelude to a period of activity and advance. When prices are up and the country is prosperous, it is always said that while preceding booms have not lasted, there are circumstances connected with this one which [are] unlike its predecessors and give assurance of permanency. The one fact pertaining to all conditions is that they will change."

The market will change. It will fall into the pothole of some great unknown unknown in a similar fashion to how the great commodity bubble of 2008 was popped by the economic crisis. It will change all of a sudden, in a shocking fashion, and in a direction that very few anticipated. Consider this fact:

.

.

In the last 10 years, natural gas has been this cheap twice. Each time, within a year, the market traded near $10. The first time was in 1q of 2000 when gasd was trading just above $2.00. by December of 2000, when it traded for $9.73.The second time was in July of 2002, when gas was trading around $2.75. By February of 2003, gas traded for $9.33.

.

.

Allow me some license to blend the statements of Secretary Rumsfeld and Mr. Dow:

"The known unknown pertaining to all market conditions is that they will change."

Sunday, August 30, 2009

Saturday, June 20, 2009

Thursday, June 11, 2009

Khurais Oilfield Opens - And Helps Us Comprehend Energy Instability

Khurais Oil Field - Ghawar's little brother - began production recently. Here is an article from the NY Times from a year ago that details the field and the development of the facility. It has been a remarkable undertaking, the scale of which should not be underestimated.

Khurais will produce 1.2 million barrels a day, which is about 1.5% of world demand (per the IEA). The IEA also conservatively estimates in the most recent World Energy Outlook that demand will grow at 1.2% per year worldwide.

Basically, we need the equivalent of 1+ Khurais each year, just to keep up with world oil demand growth. Sound like a challenge?

Alternatively, see what Forbes wrote about the Haynesville Shale...enough natural gas to last a decade...

Khurais will produce 1.2 million barrels a day, which is about 1.5% of world demand (per the IEA). The IEA also conservatively estimates in the most recent World Energy Outlook that demand will grow at 1.2% per year worldwide.

Basically, we need the equivalent of 1+ Khurais each year, just to keep up with world oil demand growth. Sound like a challenge?

Alternatively, see what Forbes wrote about the Haynesville Shale...enough natural gas to last a decade...

Wednesday, June 10, 2009

Energy and Sustainability with the CEO of Coke

Watch this between the 10 and 13 minute mark. Interesting perspective.

Monday, June 8, 2009

Tuesday, May 26, 2009

Switching Horses on Oil Strategy

The WSJ reports on big oil's quandary...can't make new capital investment in exploration cause it just don't pay...

Thunder Horse, which started up in 2008, will provide 42% of BP's incremental upstream production over the next three years, according to analysts at J.P. Morgan Chase. Unfortunately, it is also one of BP's few discoveries of such scale in recent memory. Neil McMahon of Sanford C. Bernstein calculates that less than half of BP's additions to reserves over the past five years have come through its exploration efforts.

Friday, May 22, 2009

Malcolm Gladwell on Underdogs and Inliers

Malcom Gladwell is an author I enjoy greatly. And I recently found two pieces of his that are worth your time. One is about achieving success as an underdog. The next is about successful people who get missed by the media - "inliers" in his vernacular.

From the New Yorker:

From the New Yorker:

Insurgents, though, operate in real time. Lawrence [of Arabia] hit the Turks, in that stretch in the spring of 1917, nearly every day, because he knew that the more he accelerated the pace of combat the more the war became a battle of endurance—and endurance battles favor the insurgent. “And it happened as the Philistine arose and was drawing near David that David hastened and ran out from the lines toward the Philistine,” the Bible says. “And he reached his hand into the pouch and took from there a stone and slung it and struck the Philistine in his forehead.” The second sentence—the slingshot part—is what made David famous. But the first sentence matters just as much. David broke the rhythm of the encounter. He speeded it up. “The sudden astonishment when David sprints forward must have frozen Goliath, making him a better target,” the poet and critic Robert Pinsky writes in “The Life of David.” Pinsky calls David a “point guard ready to flick the basketball here or there.” David pressed. That’s what Davids do when they want to beat Goliaths.From Sports Illustrated:

Nick Faldo [is a golf inlier]. Think about it. He wins six majors. He's the dominant golfer of the late 1980s and early 1990s. But we don't mention him in the same breath as, say, Arnold Palmer, even though Palmer only won one more major than Faldo. And why? Because Palmer had Nicklaus and Faldo had, well, Scott Hoch, Mark McNulty and John Cook. Now imagine he comes along in the late '90s and goes toe-to-toe with Tiger Woods from the beginning. All of a sudden Faldo gets immeasurably magnified by the comparison. I'm not saying he'd beat Tiger. (Are you kidding?) But he's the perfect foil. I got a tape recently of the 1996 Masters, when Greg Norman had his epic collapse on the back nine. That tournament is always explained in terms of how Norman choked, as if there were something inside him that inevitably caused him to surrender a six-stroke lead. Nonsense. Surely the key to that whole collapse is that he's paired with Faldo, and Faldo in his prime was terrifying. He was surly and tough and charismatic and emotionally and psychologically bulletproof, and I feel like he'd do a better job of getting under Tiger's skin than anyone out there right now. What's the defining fact about Faldo? His ex-girlfriend once destroyed his Porsche with a 9-iron. The corresponding fact for Woods is that his favorite band is Hootie and the Blowfish. Hootie and the Blowfish? What's Faldo's favorite band? Joy Division? Or some kind of obscure Welsh thrash band too hard core for American radio?

Peak Oil Update

Here are three presentations by Matthew Simmons, the Twilight in the Desert guy.

Mr. Simmons is a big energy bull. The jury is still out as to whether he is full of bull. But his presentations are quite compelling.

Mr. Simmons is a big energy bull. The jury is still out as to whether he is full of bull. But his presentations are quite compelling.

Thursday, April 30, 2009

Monday, April 27, 2009

LTCM Guest Lecture at MIT

One of the Long Term Capital Management folks, talking about the implosion of this fund from back in the 90's.

* The first 1:05 of the talk is "facts and fictions about the LTCM meltdown"

* Lessons learned begins at 1 hour and 6 minutes.

* Q and A at about 1:10

Tuesday, April 21, 2009

Customer Programs in Electricity

The majority of postings on this site are related to commodity markets. Why? Because I find them interesting and dynamic, and because my readers feel the same way. Commodity markets are inherently interesting because they change so quickly. Also (and this is kind of a drag), we are exposed to commodity price in our businesses.

So if the majority of postings are on the drivers of commodity prices, would it surprise you to know that I feel that commodity price fundamentals are not the most important thing that this site communicates? It is true...most of my postings are interesting and important (arguably) - but not crucial to business success.

The following post IS crucial to business success. It deals with providing customers choice and certainty. I have posted previously about how developing customer programs like budget billing, fixed price offerings, and not-to-exceed (cap) price offerings - and how these programs are integral to a business's success. Why do I feel this way? They create customer freedom to choose. Customer certainty. Customer flexibility. Customers can be offered program entry points at multiple times during the year and customers have the ability to spread their costs evenly over a number of months are the happiest customers. Per Gallon Price becomes less of a hurdle. Value is added above the delivery of the molecule into the customer tank.

Here is more proof, via Yahoo Finance:

Embracing these programs satisfy a customer need. They allow the local propane company to offer piece of mind to the customer, and make paying the heat bill feel like paying the cell phone bill, or the water bill.

In grad school, I learned that businesses should "make it easy for their customers to give them money." The more flexible our businesses become to our customers' desires, the more customers will embrace us as their supplier - regardless of price.

So if the majority of postings are on the drivers of commodity prices, would it surprise you to know that I feel that commodity price fundamentals are not the most important thing that this site communicates? It is true...most of my postings are interesting and important (arguably) - but not crucial to business success.

The following post IS crucial to business success. It deals with providing customers choice and certainty. I have posted previously about how developing customer programs like budget billing, fixed price offerings, and not-to-exceed (cap) price offerings - and how these programs are integral to a business's success. Why do I feel this way? They create customer freedom to choose. Customer certainty. Customer flexibility. Customers can be offered program entry points at multiple times during the year and customers have the ability to spread their costs evenly over a number of months are the happiest customers. Per Gallon Price becomes less of a hurdle. Value is added above the delivery of the molecule into the customer tank.

Here is more proof, via Yahoo Finance:

DALLAS (AP) -- At TXU Energy, the biggest electric company in Texas, the fastest-growing billing plan is one that lets customers lock in the price of power for one or two years.Our deregulated competition is beginning to offer flexible payment terms - not selling price but selling value to the consumer. Will our industry be early adopters of this customer service, or will our competitors build a competitive beachhead and some momentum in this regard?

"It's easier to plan that way, and I think you're saving money," says Brian Bell, an advertising salesman who signed a 2-year, fixed-price contract for electricity at the 1,500-square-foot Dallas town house he bought last year.

Other homeowners across the country are locking in prices now on electricity for summer cooling and heating oil for next winter. Heating oil prices are nearly 60 percent lower than they were at this time last year, according to Energy Department figures.

Natural gas prices have fallen as well, which not only affects the price homeowners pay for gas but the price of electricity produced by power plants that run on gas.

Embracing these programs satisfy a customer need. They allow the local propane company to offer piece of mind to the customer, and make paying the heat bill feel like paying the cell phone bill, or the water bill.

In grad school, I learned that businesses should "make it easy for their customers to give them money." The more flexible our businesses become to our customers' desires, the more customers will embrace us as their supplier - regardless of price.

Saturday, April 18, 2009

The Curve of Forward Prices

An article containing some good explanation about what the forward price curve represents can be found at DownstreamToday.com. Here is an excerpt:

Looking at the prices of long-dated oil futures can be useful as they provide the best tradable indication of the future expected price of the commodity. While long-dated futures contracts are traded less frequently than their near-month counterparts, the December contract is an exception as speculators and producers attempt to lock in or hedge oil exposure for year-end.

Oil producers use the futures prices as a key benchmark for domestic production, using the contracts to hedge current inventory or using the price to evaluate potential exploration projects.

"The forward price of crude oil is a combination of the need to fund existing stock levels and trading flows, which in turn embody price expectations," said Lawrence Eagles, global head of commodities research at JPMorgan.

While long-dated futures contracts are still much higher than the near month, a situation described as contango, the forward curve has been flattening out recently as traders have adjusted expectations after weeks worth of data from the Energy Information Administration, an Organization of Petroleum Exporting Countries meeting and bulk shipping statistics. As the curve flattens, the long-dated contracts fall at a faster rate than the near-month contract, or the near-month contract rises faster than those further out. A year-end rally could be thwarted by continued weak demand and burgeoning supplies. Oil demand is forecast to fall to the lowest level in five years, according to the Energy Information Administration. U.S. crude oil inventories are at 18-year highs.

Thursday, April 16, 2009

A Fantasticly Entertaining Waste of Time

The Washington Post held its third annual Peep-Art Competition recently.

HERE are the 20 top reader diorama submissions.

HERE are the 20 top reader diorama submissions.

OPEC Oil Market Report for March

Monthly Oil Market Highlights in an audio podcast, as OPEC sees them...

* Outlook is Bearish as world GDP is being revised downward.

* World GDP is contracting by about 1%

* Supply growth is slowing, too

* Days of forward supply (at 60 days) are the highest they have been in 15 years

* Outlook is Bearish as world GDP is being revised downward.

* World GDP is contracting by about 1%

* Supply growth is slowing, too

* Days of forward supply (at 60 days) are the highest they have been in 15 years

Southwest Reports that Fuel Hedging Program Creates More Losses

From Southwest's 10Q, released today.

More importantly for propane and heating oil marketers, though, check out that they bought long dated CALLS to protect their position. They weren't afraid to spend the premium for the insurance that the calls provide. Also, they view their fuel risk position as a portfolio - and seem to be willing to enter into a number of strategies to achieve their goal. Finally, they have a model that they use that can help them plan what costs will be due to the hedging tools they hold in their portfolio. These are the things that every propane and heating oil marketer should be doing to manage their risk and fine tune their business.

“We benefited from significantly lower year-over-year economic jet fuel costs in first quarter 2009. Even with $65 million in unfavorable cash settlements from derivative contracts, our first quarter 2009 economic jet fuel costs decreased 16.2 percent to $1.76 per gallon. With oil prices rising, we have begun to rebuild our 2009 and 2010 hedge positions, using purchased call options, to provide protection against significant fuel price spikes. These new positions present no additional exposure to cash collateral requirements. Furthermore, we have modified our major fuel hedge counterparty agreements to allow us to use collateral other than cash to limit our cash collateral exposure to comfortable levels. Based on our second quarter derivative position and market energy prices as of April 14, 2009, we currently anticipate our second quarter 2009 economic jet fuel costs, including taxes, to be in line with first quarter 2009 (or the $1.75 per gallon range).”I am partial to the SWA business model and corporate culture. It has proven its competitive advantage in the best of times and the worst of times. Its team members are friendly and motivated, and its management is aggressive in attacking opportunity. Plus...they are active fuel price speculators. Their hedging program has earned them kudos from the national media, and has been written about on this site several times. But unless your fuel price speculation program is run by Bernie Madoff (pre-ponzi), even the best traders and economists are going to lose once in a while.

The Company has derivative contracts in place for approximately 50 percent of its second quarter 2009 estimated fuel consumption, capped at a weighted average crude-equivalent price of approximately $66 per barrel; approximately 40 percent for the remainder of 2009 capped at a weighted average crude-equivalent price of approximately $71 per barrel; and approximately 30 percent in 2010 capped at a weighted average crude-equivalent price of approximately $77 per barrel. The Company has modest fuel hedge positions in 2011 through 2013. The current market value (as of April 14, 2009) of its net fuel derivative contracts for 2009 through 2013 reflects a net liability of approximately $950 million.

More importantly for propane and heating oil marketers, though, check out that they bought long dated CALLS to protect their position. They weren't afraid to spend the premium for the insurance that the calls provide. Also, they view their fuel risk position as a portfolio - and seem to be willing to enter into a number of strategies to achieve their goal. Finally, they have a model that they use that can help them plan what costs will be due to the hedging tools they hold in their portfolio. These are the things that every propane and heating oil marketer should be doing to manage their risk and fine tune their business.

If SWA management needs a post 10q pick-me-up, I am sure that they could step on board one of their planes with this industrious and talented flight attendant.

Monday, April 13, 2009

Sunday, April 12, 2009

Natural Gas Basics

This is a 4-page analysis of simple supply and demand in the natural gas sector. It was released by the EIA last week, and is a good basic overview.

Friday, April 10, 2009

Thursday, April 9, 2009

Causes of the Oil Shock

This article is from Econbrowser, a blog from Dr. James Hamilton - a professor from the University of San Diego.

It discusses a paper he wrote on the causes of the oil price rally of 2007-2008. It is formal and academic, and there are charts and formulas. But here is the bottom line: Dr. Hamilton agrees with my thesis regarding the rally. Dr Hamilton states:

It discusses a paper he wrote on the causes of the oil price rally of 2007-2008. It is formal and academic, and there are charts and formulas. But here is the bottom line: Dr. Hamilton agrees with my thesis regarding the rally. Dr Hamilton states:

"Growth in world income was the primary cause behind an increase in world petroleum consumption of 5 million barrels per day between 2003 and 2005, a 6% increase over the two years. The next two years (2006 and 2007) saw even faster economic growth (10.1% cumulative two-year growth), with Chinese oil consumption alone increasing 870,000 barrels per day. Yet between 2005 and 2007, global oil production stagnated.My article (from early January) is here.

The cool thing is that Dr. Hamilton and I agree on the causes. He builds better looking models, though.

Wednesday, April 8, 2009

New Clear Energy

Is Nuclear Energy the Answer to our power-centric lifestyle?

Here is an opinion article from the Wall Street Journal that details the pro and con.

Tuesday, April 7, 2009

Monte Carlo Simulations In Baseball

I remember playing strat-o-matic baseball with my older brothers as a kid. This is just as cool.

Monday, April 6, 2009

In Defense of Derivatives

From the opinion page of the Wall Street Journal, by Rene Stultz:

From the perspective of Main Street companies, derivatives are not just about high finance, quants and politics, but about investing in America's core industries, jobs and economic recovery. Companies find that over-the-counter derivatives are essential to their day-to-day operations. Derivatives help insulate them from risk, which allows them to borrow capital at better prices than they would otherwise. And derivatives are more useful than ever in these days of unusual volatility in financial markets.

For example, not being able to hedge currency risk through the use of a derivative can leave a company exposed to fluctuations in currency markets. Without derivatives companies could see movements in exchange rates turn a profitable export contract into a money-losing agreement.

In its current annual report, Caterpillar Inc. makes the case for why it relies on derivatives: "Our risk management policy . . . allows for the use of derivative financial instruments to prudently manage foreign currency exchange rate, interest rate, commodity price and Caterpillar stock price exposures...."

Our businesses need derivatives. Most of us choose to drive cars even though they sometimes crash. But we also insist that cars are made as safe as it makes economic sense for them to be, and that speed limits and other rules of the road are enforced. The same logic should apply to derivatives.

Declarations about Certainty and Questions about Nuance

Over the past couple of weeks I have posted several pieces that are skeptical in tone, including (especially) my post on Experts. This posting must have touched a nerve, as I received more comments about this posting than any other prior post on the site. It seems folks thought that was ironic for someone who claims himself to be a commodity market expert to dis experts on his site.

(By the way, one of the signs that my blog is gaining traction is that readers contact me now to provide their opinions. FANTASTIC! And THANKS!! I am lucky to have readers who care, and all comments are appreciated. If something in particular strikes you, leave some comments at the end of the posting for others to consider. Heck, most of the readers of this blog are smarter than I am - so you will probably teach me (and everyone else) something significant.)

Allow me to move back to the "Experts" subject, though. Indeed, I do encourage everyone to have a robust skepticism of what they think they "know". I side with Nicholas Taleb in this regard - in The Black Swan he says that the market is far more random than folks want to believe. There are analysts, marketers, and consultants throughout the world of stocks and commodities that make recommendations on how you (Mr. Third Party) should allocate your assets or time the market. Do they know with any reliable certainty? Of course not, otherwise they would keep their mouth shut and do what they are recommending with their own money.

However, just because the markets are more random than we perceive or want them to be does not mean that they are ALWAYS random. There are times when folks can execute a winning trade through research and discipline (and serendipity).

Unfortunately, the fact that the markets are random does not excuse us from having bottom line accountability to our banker (or our wife or our employees or our manager or our owner or our shareholders). It is the game we play, and those are the cards we have been dealt. The fact that markets is difficult or irrational does not excuse a business owner from making educated decisions.

Working with a market professional whom you trust can help you stay away from the cycle of greed, hope, and fear. Professionals can advise you on on the fundamental, seasonal, and technical factors in play in the market. Most importantly, professionals can help you discern the questions to ask yourself about your business. When you understand the questions, you can define the answers...and when you know the answers with certainty, decisions can be made with confidence. It is lonely (and a little scary) to make those decisions in solitude.

I appreciate the role of experts. But we must ask ourselves if those experts are engaging speakers that make declarative statements about certainties or whether they are humble market professionals that ask questions about nuance.

Any thoughts???

(By the way, one of the signs that my blog is gaining traction is that readers contact me now to provide their opinions. FANTASTIC! And THANKS!! I am lucky to have readers who care, and all comments are appreciated. If something in particular strikes you, leave some comments at the end of the posting for others to consider. Heck, most of the readers of this blog are smarter than I am - so you will probably teach me (and everyone else) something significant.)

Allow me to move back to the "Experts" subject, though. Indeed, I do encourage everyone to have a robust skepticism of what they think they "know". I side with Nicholas Taleb in this regard - in The Black Swan he says that the market is far more random than folks want to believe. There are analysts, marketers, and consultants throughout the world of stocks and commodities that make recommendations on how you (Mr. Third Party) should allocate your assets or time the market. Do they know with any reliable certainty? Of course not, otherwise they would keep their mouth shut and do what they are recommending with their own money.

However, just because the markets are more random than we perceive or want them to be does not mean that they are ALWAYS random. There are times when folks can execute a winning trade through research and discipline (and serendipity).

Unfortunately, the fact that the markets are random does not excuse us from having bottom line accountability to our banker (or our wife or our employees or our manager or our owner or our shareholders). It is the game we play, and those are the cards we have been dealt. The fact that markets is difficult or irrational does not excuse a business owner from making educated decisions.

Working with a market professional whom you trust can help you stay away from the cycle of greed, hope, and fear. Professionals can advise you on on the fundamental, seasonal, and technical factors in play in the market. Most importantly, professionals can help you discern the questions to ask yourself about your business. When you understand the questions, you can define the answers...and when you know the answers with certainty, decisions can be made with confidence. It is lonely (and a little scary) to make those decisions in solitude.

I appreciate the role of experts. But we must ask ourselves if those experts are engaging speakers that make declarative statements about certainties or whether they are humble market professionals that ask questions about nuance.

Any thoughts???

Saturday, April 4, 2009

China Owns Too Many Dollars

One of my favorite articles over the last several years was "The $1.4 Trillion Question" from the Atlantic Monthly. It discussed how the Chinese were amassing huge amounts of dollar denominated assets, and asked the question "what will happen next?" or maybe "what might go on to get the Chinese to be sellers of their stash of US dollars?"

Paul Krugman opined on this subject yesterday in the New York Times (15 months after the Atlantic Monthly piece was published). Here is a piece of that article:

I figured the Chinese knew what they were doing when they were buying all those dollars. I figured they had the best and brightest of the People's Republic in a quiet and stoic bureau somewhere in the governmental center of Beijing, and that those folks were planning for Chinese economic dominance on the grandest scale (like so many drummers at the Olympics Opening Ceremonies).

Maybe it was all an economic accident. And the global economic quandary for our times....

Paul Krugman opined on this subject yesterday in the New York Times (15 months after the Atlantic Monthly piece was published). Here is a piece of that article:

And the Chinese DO have a problem. They have amassed a position in US dollars that is so large that it does not have ample liquidity for an orderly exit. That's just crazy...US Dollars are the most liquid asset on Earth! This isn't a tertiary market like pork bellies or frozen concentrated orange juice, Mortimer - it is the sovereign currency of the largest economy in the world.Some background: In the early years of this decade, China began running large trade surpluses and also began attracting substantial inflows of foreign capital. If China had had a floating exchange rate — like, say, Canada — this would have led to a rise in the value of its currency, which, in turn, would have slowed the growth of China’s exports.

But China chose instead to keep the value of the yuan in terms of the dollar more or less fixed. To do this, it had to buy up dollars as they came flooding in. As the years went by, those trade surpluses just kept growing — and so did China’s hoard of foreign assets......Was there a deep strategy behind this vast accumulation of low-yielding assets? Probably not. China acquired its $2 trillion stash — turning the People’s Republic into the T-bills Republic — the same way Britain acquired its empire: in a fit of absence of mind.

And just the other day, it seems, China’s leaders woke up and realized that they had a problem.

I figured the Chinese knew what they were doing when they were buying all those dollars. I figured they had the best and brightest of the People's Republic in a quiet and stoic bureau somewhere in the governmental center of Beijing, and that those folks were planning for Chinese economic dominance on the grandest scale (like so many drummers at the Olympics Opening Ceremonies).

Maybe it was all an economic accident. And the global economic quandary for our times....

Wednesday, April 1, 2009

Kamikaze Spending In Japan

The Wall Street Journal Asia Edition has a short editorial today regarding the stimulus effort undertaken by the Japanese government:

Prime Minister Taro Aso yesterday ordered his government to draw up yet another stimulus package to buoy his sinking economy. In an interview with the Journal's Yuka Hayashi published on Monday, Economy and Finance Minister Kaoru Yosano said the program will "far exceed" the 2% of GDP recommended by the International Monetary Fund and will include measures to boost credit, maintain employment and strengthen the social safety net.

This takes fiscal profligacy to a new level. Mr. Aso's Administration and its immediate predecessor have already rolled out about 1.5% of GDP in new spending since the financial crisis hit last year. As of today, Tokyo estimates government debt-to-GDP is at 157.5%. The OECD puts that figure higher, around 180%. Mr. Aso said yesterday he would "not hesitate" to issue bonds to pay for his plans.

I mentioned in the most recent 4+1 commentary that the US dollar stands to be the "least worst soverign currency." Of course, 2 days later the government announced a plan to buy a trillion dollars of paper and the dollar took its biggest one-day hit in almost 50 years. I am still bullish the dollar - not necessarily because of the strength of the domestic economy, but rather because of the weakness of other economies worldwide. The stimulus of a slowing Japanese economy is another example of worldwide weakness.

Monday, March 30, 2009

Who is your Propane or Heating Oil Expert?

The Jim Cramer - John Stewart debate has lit up the national discourse on a good topic - the value of an expert. Jim Cramer is an expert to a section of the stock buying public - but his advice hasn't worked out so well of late. There are only a few folks that have done well in this market, and those investors are to busy counting their money to do a TV show.

But this does highlight a few valid questions - How do we choose the people we trust? And what qualities make a person an expert?

Last week, Nicholas Kristof wrote an excellent op-ed piece in the NY Times. It was on the "Dr. Fox effect." The whole article is worth a read, the following is an excerpt:

Ben Stein goes further to put this in perspective in another NY Times editorial:

Reevaluate who you trust. What questions do they ask? Do they understand your balance sheet, your customer base, and your business processes? If they don't, they might be a "Dr. Fox" - a false expert.

The value of a market expert is not in helping you make only good decisions. The value of a market expert is to help you understand - in advance - the impact of a bad decision, and then to assist you in steering your business clear of the kind of mistake that it cannot afford.

Before you make your next risk management decision, consider the trader's axiom "The market can remain illogical far longer than individuals can remain solvent." If your purchase decision can withstand the clarity granted by this statement, then it is probably a hedge. If not, you might wind up as frustrated with your "expert" advisor as Stewart was with Cramer.

But this does highlight a few valid questions - How do we choose the people we trust? And what qualities make a person an expert?

Last week, Nicholas Kristof wrote an excellent op-ed piece in the NY Times. It was on the "Dr. Fox effect." The whole article is worth a read, the following is an excerpt:

Scary, huh? A good presenter = an expert. Or maybe an "engaging talking head" = an expert (Jim Cramer, maybe?).The best example of the awe that an “expert” inspires is the “Dr. Fox effect.” It’s named for a pioneering series of psychology experiments in which an actor was paid to give a meaningless presentation to professional educators.

The actor was introduced as “Dr. Myron L. Fox” (no such real person existed) and was described as an eminent authority on the application of mathematics to human behavior. He then delivered a lecture on “mathematical game theory as applied to physician education” — except that by design it had no point and was completely devoid of substance. However, it was warmly delivered and full of jokes and interesting neologisms.

Afterward, those in attendance were given questionnaires and asked to rate “Dr. Fox.” They were mostly impressed. “Excellent presentation, enjoyed listening,” wrote one. Another protested: “Too intellectual a presentation.”

Ben Stein goes further to put this in perspective in another NY Times editorial:

Humans can’t consistently pick the right stocks or call markets, foretell political or geopolitical events or successfully predict changes in interest rates or commodity prices.So where does this leave us in our search for market wisdom? What is a retailer to do when he or she realizes that no one can predict the future with consistency and that "the folks that know aren't talking?"Life is far too complex and baffling for the minds of mortals to understand it as it happens, let alone to predict it accurately. (I am mindful of how Professor Friedman, a true supernova of brilliance, said of economic forecasting, “If you’re going to predict, predict often.”) Some humans shine like dazzling stars when their predictions turn out to be true, but those same humans can’t ever be counted on to replicate the feats regularly.

Yet, we cry out for someone to tell us the future, like children who want to hear the end of the story. When Mr. Cramer tries to satisfy that need, he is doing no more than answering a deep human wish. But he — and everyone else in a similar situation — should make it clear that these are no more than opinions and guesses, which could easily be wrong and often are.

This is not just boilerplate. This is life. The way it is.

Reevaluate who you trust. What questions do they ask? Do they understand your balance sheet, your customer base, and your business processes? If they don't, they might be a "Dr. Fox" - a false expert.

The value of a market expert is not in helping you make only good decisions. The value of a market expert is to help you understand - in advance - the impact of a bad decision, and then to assist you in steering your business clear of the kind of mistake that it cannot afford.

Before you make your next risk management decision, consider the trader's axiom "The market can remain illogical far longer than individuals can remain solvent." If your purchase decision can withstand the clarity granted by this statement, then it is probably a hedge. If not, you might wind up as frustrated with your "expert" advisor as Stewart was with Cramer.

Tuesday, March 24, 2009

The Emotions of the Market: Hope

In the 1930's, the economist John Maynard Keynes used the term "animal spirits" to describe human emotion in the marketplace. In the last 10 years, the Nobel Prize has been awarded to economists from the University of Chicago School of Business that have pioneered in the field of Behavioral Finance.

Emotion is not to be discounted in the market. And it plays a huge role in the decision to enter a fixed price contract. There are three main emotions that effect the buying decision, and they work in coordination with each other to help create a poor decision. These are the emotions of Greed, Hope, and Fear. They are not your friends, and when you detect them in your mind they should be dispatched with extreme prejudice. I would venture to guess that HOPE is an emotion that is at play in your mind today.

Consider the market context that we have recently experienced.

Emotion is not to be discounted in the market. And it plays a huge role in the decision to enter a fixed price contract. There are three main emotions that effect the buying decision, and they work in coordination with each other to help create a poor decision. These are the emotions of Greed, Hope, and Fear. They are not your friends, and when you detect them in your mind they should be dispatched with extreme prejudice. I would venture to guess that HOPE is an emotion that is at play in your mind today.

Consider the market context that we have recently experienced.

- In July, prices were sitting at all time highs ($147/bbl on NYMEX crude)

- But by November they had fallen to $37 - $40/bbl MORE than even the most bearish observer thought they could

- The brutality of the fall caused folks all over the industry to examine their existing positions closely, they needed to make sure their positions were flat. Additionally, there were margin calls to work through. This period of time was very busy, as folks were attending to pressing business that could not be put off.

- However, it was also (in retrospect) the best time to lock in some product. The wholesale price that was available in the market at this time was one that could be used as a base for a 2009-2010 fixed price program. A margin could be added, and the retail customer would have been interested. A large segment of marketers passed on this opportunity, though...it just wasn't a good time for them to make that leap.

- Propane prices are now 30 cents above the price that was available in November.

- Over the last month or so, folks have been thinking about layering into a piece of prebuy. Seasonally, it makes sense to do so as the market often trades on its annual lows in the first quarter.

- Last week, an unexpected fundamental (news of the Treasury's plan to buy $1.0 trillion is debt) caused historic weakness in the dollar, and therefore spiked commodity prices across the board (energy prices included).

- Those folks that were still waiting to lock in a piece of fixed price product find themselves in a state of shell shock, confused by the market's fluctuations and not knowing what to do.

- Here is where the HOPE sets in:

It becomes the natural human reaction to wait for a while before pulling the trigger on a contract. Marketers in this situation are HOPING that the price moves lower and that they are able to get the price they could have gotten previously. They may wind up HOPING in that way for several months, as the price continues to move higher.

Whether you should buy now or wait is really a question that is dependent upon your unique business, customer base, and target margin structure. No one should ever give a blanket purchase recommendation to customers, although there are consultants that do so.

However, what an independent third party can do is offer perspective and encourage a balance between emotional and rational. Is there too much HOPE in your program? If so, consider buying the piece you might have missed out on last week.

Whether you should buy now or wait is really a question that is dependent upon your unique business, customer base, and target margin structure. No one should ever give a blanket purchase recommendation to customers, although there are consultants that do so.

However, what an independent third party can do is offer perspective and encourage a balance between emotional and rational. Is there too much HOPE in your program? If so, consider buying the piece you might have missed out on last week.

Monday, March 23, 2009

Wednesday, March 18, 2009

Tuesday, March 17, 2009

Campbells Soup Reports Hedges as a Drag on Earnings

Just to demonstrate that folks in other industries "guess wrong" too...

Hat tip to DealBreaker.

But do you see the concept of sticky margins in action?CHICAGO (Reuters) - Consumers looking for relief from rising food prices are not likely to see any price cuts soon from Campbell Soup Co (CPB), which is still dealing with high commodity costs under previously set contracts.

Sales of the world's largest soup maker have been helped by consumers eating more at home, and the company sees little need to cut prices, especially while margins remain under pressure, CEO Douglas Conant said at the Reuters Food and Agriculture Summit in Chicago.

"Quite frankly, sales are growing, our marketplace presence is growing, consumer purchases are actually growing faster than sales," Conant said. "Clearly we're having a good year, we've had the best year in soup that I've experienced in my nine years here."

"So it's not likely we're going to be reducing prices in the near term."

But Conant also said that strategy could change if commodity prices come down and margins improve.

Like many food companies, Campbell locks in some costs for grains and other ingredients through commodity hedges. The company hedged some commodities when prices were at historic highs last year and those hedges run until July, Conant said.

"As those hedges come off and if our margins start to turn around, then we'll reconsider that, but that's premature to talk about," Conant said about the possibility of lowering prices.

"We're hopeful our margins will improve in the second half but for the full year, at best they'll be flat," Conant said. "So we won't recover everything we lost in the first half."

Hat tip to DealBreaker.

Monday, March 16, 2009

4+1 Market Commentary

It has been a while since I last posted a 4+1 market commentary - a posting that is meant to tie together and make sense of the different postings on this site. Truth be told, it isn't because I didn't have stuff to write about. I can always come up with something to talk about (ask my wife).

Instead, I had a technology problem. At the end of the last 4+1 I mentioned that my next 4+1 post would be a video blog posting. That was the goal. But it was "all hat and no cattle." I didn't have my technology worked out, and trying to install the audio and video technology cause a devastating error on my computer. It was called a "kernel stack" error. Being a finance guy, I really don't know what a kernel stack is. Nor do I quite understand why kernels would need to be stacked. But I do know if your kernels are not stacked you won't be happy with the outcome.

I was minding my own business and stringing the USB cord one minute, and the next I was looking at the "blue screen of death" and contemplating the complete system restore. Wow, what a mess! I was out of commission for three days. If I could offer the readers of this site just one humble piece of advice, I would recommend you make sure all kernels are stacked appropriately at all times. The video post is coming...after I restack my kernels, and do whatever I need to do to make sure that what happened NEVER happens again.

Now...on to business. I will touch on 4 important market factors, as well as one thing that does not matter at all.

1) The Changing Face of OPEC

Russia is an observer, and Brazil was entreated to join but refused. Economies that rely on petrodollars as a significant economic driver are aligning together. OPEC becomes even more important in the future for these economies, because petrodollars lubricate the wheels of government. Petroeconomies are typically run by petro-dictators, and dictatorship (or autocracy) is easiest in a climate of economic plenty. The lower classes are happy with the government when there are petrodollars to go around - and they are more unsettled when they do not have jobs or when the economies have to cut back on building projects or social projects.

Compliance is a big thing, because OPEC saying it will cut and OPEC actually cutting production are really two different things. However, the most recent round of cuts has actually gone better (from a compliance standpoint) than I had expected. To put this in perspective, right now OPEC members are receiving about a quarter of the oil revenues that they received this summer, due to the falling price of crude and the production cuts that have been announced. When you think about it this way, it makes Oman and the UAE sound a bit like Las Vegas - having taken a massive cut in the revenue source that the economy was built upon.

OPEC's ability to constrain supply is bullish. Maybe not now - but when it begins to matter again.

2) Demand is Driving

Domestic gasoline demand is UP year over year. The mainstream media might want you hold yourself up in a tornado shelter because Armageddon is nigh...but it is not. Folks are driving more this year than they did last year. And we must remember that, due to EPA regulations, there have been no new refineries built in the US in 30 years. There is a supply/demand imbalance regarding domestic refining capacity - and that imbalance will show itself again this summer. Look for the crack spreads to widen, and potentially apply upward pressure to the crude complex, as the marketplace finds itself in the driving season.

Strong demand for finished products is bullish to the market.

3) The Least Worst Sovereign Currency

Democracy and Capitalism are the perfect parlay - I will bet on the resilience of both of them. When the government exercises restraint and does not attempt to meddle or socially engineer solutions, the independent American businessman solves problems. He/She allocates capital efficiently and grows his/her business. Growth in business means growth in economic value - and growth in economic value is the way we get out of the recessionary funk in which we currently find ourselves mired.

Other countries don't exactly work like that. Government tries, but one or one hundred bureaucrats cannot allocate capital as efficiently as businessmen like you and me. China is trying, of course. But this op-ed piece from the India Times eloquently states my point - when the world economy is stressed, look to America to lead the recovery - due to the resilience of the American businessperson.

Due to this resilience, the dollar index should maintain its strength against other currencies. A strong dollar makes crude and other commodities priced in dollars cheaper (because a dollar goes further when buying some). This is neutral to bearish for energy prices.

4) Oil on a Fulcrum

The incremental cost of production for the next barrel is somewhere above $60/bbl. So when the cash price is below $60, no new production cash flows. More importantly, plans get mothballed, exploration ships get dry docked, and crews get sent home. Major oil projects take years to plan and develop in good economies. But allowing all the assembled physical assets, inertia, and human capital to disburse back to their home bases mean that the supply will no be there when it is needed, and it will take years to bring these hydrocarbons to market. Therefore, the more time the market spends below the $60-$65 threshold, the more violent and pronounced the spike will be.

China knows. They are on a buying spree, grabbing commodity assets throughout eastern Asia and the Pacific rim. Billions are being spent so that China is secure and well positioned for further worldwide demand-based uncertainty.

Are we at peak oil? Personally, I don't think so. However, demand is increasing as economies modernize. And it takes a whole lot of infrastructure to slake the world's energy thirst. I my mind, the move to $147 can be repeated, and may just be an opening act for the volatility and price moves to come, as the new Asian middle class develops a liking for the hydrocarbon intensive goods and services (corn, cars, plastic stuff, etc.)

Crude oil being below the cost of production is bullish for energy prices.

+1) The one thing folks should be ignoring: Banks and Credit

The credit market is healing, and the Federal Reserve has demonstrated a willingness to print money to insure the solvency of the system. Markets are looking more positive in a number of ways. And each day that goes by gives the large financial institutions more time to de-leverage and heal themselves. Sure, there are pockets of the domestic market that will take a long time to heal (California, Phoenix, coastal Florida) but in a year, our market will be focusing on a new problem - it will most likely not be the credit markets.

Daily news headlines regarding banks and credit markets should not a reason for the energy markets to lose 10% or more in a day (like has happened in the last few months).

-------

If you like or dislike this stuff - my analysis - feel free to leave an anonymous post comment.

Instead, I had a technology problem. At the end of the last 4+1 I mentioned that my next 4+1 post would be a video blog posting. That was the goal. But it was "all hat and no cattle." I didn't have my technology worked out, and trying to install the audio and video technology cause a devastating error on my computer. It was called a "kernel stack" error. Being a finance guy, I really don't know what a kernel stack is. Nor do I quite understand why kernels would need to be stacked. But I do know if your kernels are not stacked you won't be happy with the outcome.

I was minding my own business and stringing the USB cord one minute, and the next I was looking at the "blue screen of death" and contemplating the complete system restore. Wow, what a mess! I was out of commission for three days. If I could offer the readers of this site just one humble piece of advice, I would recommend you make sure all kernels are stacked appropriately at all times. The video post is coming...after I restack my kernels, and do whatever I need to do to make sure that what happened NEVER happens again.

Now...on to business. I will touch on 4 important market factors, as well as one thing that does not matter at all.

1) The Changing Face of OPEC

Russia is an observer, and Brazil was entreated to join but refused. Economies that rely on petrodollars as a significant economic driver are aligning together. OPEC becomes even more important in the future for these economies, because petrodollars lubricate the wheels of government. Petroeconomies are typically run by petro-dictators, and dictatorship (or autocracy) is easiest in a climate of economic plenty. The lower classes are happy with the government when there are petrodollars to go around - and they are more unsettled when they do not have jobs or when the economies have to cut back on building projects or social projects.

Compliance is a big thing, because OPEC saying it will cut and OPEC actually cutting production are really two different things. However, the most recent round of cuts has actually gone better (from a compliance standpoint) than I had expected. To put this in perspective, right now OPEC members are receiving about a quarter of the oil revenues that they received this summer, due to the falling price of crude and the production cuts that have been announced. When you think about it this way, it makes Oman and the UAE sound a bit like Las Vegas - having taken a massive cut in the revenue source that the economy was built upon.

OPEC's ability to constrain supply is bullish. Maybe not now - but when it begins to matter again.

2) Demand is Driving

Domestic gasoline demand is UP year over year. The mainstream media might want you hold yourself up in a tornado shelter because Armageddon is nigh...but it is not. Folks are driving more this year than they did last year. And we must remember that, due to EPA regulations, there have been no new refineries built in the US in 30 years. There is a supply/demand imbalance regarding domestic refining capacity - and that imbalance will show itself again this summer. Look for the crack spreads to widen, and potentially apply upward pressure to the crude complex, as the marketplace finds itself in the driving season.

Strong demand for finished products is bullish to the market.

3) The Least Worst Sovereign Currency

Democracy and Capitalism are the perfect parlay - I will bet on the resilience of both of them. When the government exercises restraint and does not attempt to meddle or socially engineer solutions, the independent American businessman solves problems. He/She allocates capital efficiently and grows his/her business. Growth in business means growth in economic value - and growth in economic value is the way we get out of the recessionary funk in which we currently find ourselves mired.

Other countries don't exactly work like that. Government tries, but one or one hundred bureaucrats cannot allocate capital as efficiently as businessmen like you and me. China is trying, of course. But this op-ed piece from the India Times eloquently states my point - when the world economy is stressed, look to America to lead the recovery - due to the resilience of the American businessperson.

Due to this resilience, the dollar index should maintain its strength against other currencies. A strong dollar makes crude and other commodities priced in dollars cheaper (because a dollar goes further when buying some). This is neutral to bearish for energy prices.

4) Oil on a Fulcrum

The incremental cost of production for the next barrel is somewhere above $60/bbl. So when the cash price is below $60, no new production cash flows. More importantly, plans get mothballed, exploration ships get dry docked, and crews get sent home. Major oil projects take years to plan and develop in good economies. But allowing all the assembled physical assets, inertia, and human capital to disburse back to their home bases mean that the supply will no be there when it is needed, and it will take years to bring these hydrocarbons to market. Therefore, the more time the market spends below the $60-$65 threshold, the more violent and pronounced the spike will be.

China knows. They are on a buying spree, grabbing commodity assets throughout eastern Asia and the Pacific rim. Billions are being spent so that China is secure and well positioned for further worldwide demand-based uncertainty.

Are we at peak oil? Personally, I don't think so. However, demand is increasing as economies modernize. And it takes a whole lot of infrastructure to slake the world's energy thirst. I my mind, the move to $147 can be repeated, and may just be an opening act for the volatility and price moves to come, as the new Asian middle class develops a liking for the hydrocarbon intensive goods and services (corn, cars, plastic stuff, etc.)

Crude oil being below the cost of production is bullish for energy prices.

+1) The one thing folks should be ignoring: Banks and Credit

The credit market is healing, and the Federal Reserve has demonstrated a willingness to print money to insure the solvency of the system. Markets are looking more positive in a number of ways. And each day that goes by gives the large financial institutions more time to de-leverage and heal themselves. Sure, there are pockets of the domestic market that will take a long time to heal (California, Phoenix, coastal Florida) but in a year, our market will be focusing on a new problem - it will most likely not be the credit markets.

Daily news headlines regarding banks and credit markets should not a reason for the energy markets to lose 10% or more in a day (like has happened in the last few months).

-------

If you like or dislike this stuff - my analysis - feel free to leave an anonymous post comment.

Wednesday, March 11, 2009

What Do Bananas and Fixed Price Positions Have In Common?